Investors Realty tracks commercial real estate sales greater than $500,000. The following graphs highlight a few of the existing market trends we are seeing in the greater Omaha area.

Investors Realty tracks commercial real estate sales greater than $500,000. The following graphs highlight a few of the existing market trends we are seeing in the greater Omaha area.

SUMMARY OF TRENDS (2021-2025)

![]()

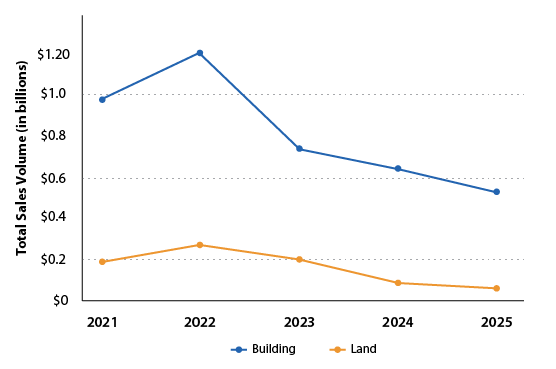

- Building Sales: The market saw a significant peak in 2022 with a total volume of $1.20 billion across 267 transactions. Since then, volume has contracted annually, returning to more typical levels and ending 2025 at $531 million. The decline represents broader economic conditions rather than a drop in underlying demand.

- Land Sales: Similar to buildings, land sales peaked in 2022 at $271.8 million. There was a sharp decline in land acquisition activity starting in 2024, with only 27 major transactions ($>500k) recorded in 2025.

- Sector Highlights:

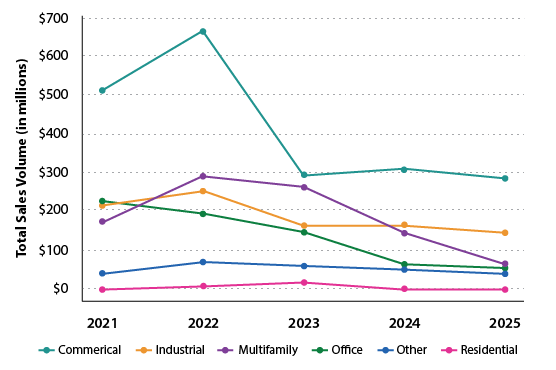

- Commercial: Consistently the highest volume sector, though it saw a ~50% drop from its 2022 peak.

- Multifamily: Experienced a surge in 2022-2023 but saw a significant pullback in 2025, dropping to roughly $65 million in volume.

- Industrial: Remained the most resilient sector, maintaining a more consistent transaction volume compared to Office or Multifamily. Page 1 has our full Industrial Market Report.

- Office: Continues a downward trend in volume, falling from $226 million in 2021 to $54.6 million in 2025. See our Office Market Report on page 6 for more insight.

- Omaha Commercial Real Estate: Navigating the “New Normal” (2021–2025)

- The Omaha commercial real estate market (CRE) has undergone a significant transformation over the past five years, moving from a period of record-breaking frenzy into a more calculated, “user-driven” environment. After reaching a historic high-water mark in 2022 with over $1.47 billion in total transaction volume (for deals over $500k), the market has since moderated as it grapples with a shifting macroeconomic landscape.

- The 2022 Peak and the “Interest Rate Lag”

- Our data reveals that 2022 was the definitive peak for Omaha CRE. This surge was largely driven by a “last call” for low-interest-rate financing; many of the landmark deals that closed that year were likely at rates locked in late 2021. As the Federal Reserve aggressively raised rates throughout 2023 and 2024, we saw the inevitable “Bid-Ask Gap” widen. Sellers held onto 2022 valuations while buyers faced significantly higher borrowing costs. That gap led to a period of price discovery, and total sales volume settled around $531 million

by the end of 2025.

- Our data reveals that 2022 was the definitive peak for Omaha CRE. This surge was largely driven by a “last call” for low-interest-rate financing; many of the landmark deals that closed that year were likely at rates locked in late 2021. As the Federal Reserve aggressively raised rates throughout 2023 and 2024, we saw the inevitable “Bid-Ask Gap” widen. Sellers held onto 2022 valuations while buyers faced significantly higher borrowing costs. That gap led to a period of price discovery, and total sales volume settled around $531 million

- Omaha’s Secret Weapon: The Owner-User

- While institutional investors often steal the headlines, the true backbone of the Omaha market has been the owner-user. Throughout the last five years, local business owners consistently out-transacted investors. In 2025 alone, there were nearly 55% more user-led transactions than investor deals. Unlike institutional capital that may sit on the sidelines during market volatility, Omaha’s local business base continues to buy out of operational necessity – expanding footprints, utilizing 1031 exchanges, or seeking the long-term stability that comes from owning their own real estate.

- A Tale of Two Sectors: Industrial vs. Office

- The data highlights a stark divergence between sectors. The Office sector continues to face structural headwinds, with transaction volume sliding from $226 million in 2021 to just $54 million in 2025 – a reflection of the national shift toward hybrid work models. Conversely, the Industrial sector has emerged as the market’s most resilient asset class. Leveraging Omaha’s strategic position as a Midwest logistics hub on the I-80 corridor, Industrial volume remained remarkably stable even as other sectors cooled, supported by consistent demand for warehouse and flex space.

- The Multifamily Cooling Period

- The Multifamily sector, which saw a massive influx of out-of-state capital in 2022 and 2023, has entered a cooling-off phase. After peaking at nearly $290 million in 2022, volume dropped to $65 million in 2025. This sector is the most sensitive to the “double whammy” of rising interest rates and surging insurance premiums, both of which compress Net Operating Income (NOI). As the market resets, we expect activity to remain focused on high-quality assets with stable occupancy.

![]()

The Bottom Line: While the headline volume numbers have come down from their post-pandemic highs, Omaha remains a fundamentally sound market. The transition from speculative investment to user-based stability suggests a healthier, more sustainable foundation for the years ahead.

This article appeared in our company newsletter in March 2026. Please click here to download the entire newsletter.