By John Heine, CCIM, JD

By John Heine, CCIM, JD

The multifamily market continues to prosper in the Omaha Metro area. According to both CoStar and Institute of Real Estate Management (IREM) data, Omaha is hovering around a 95 percent occupancy rate and has been at that level or higher since 2012. Rent growth has been double Omaha’s historical average, ranging between 2 percent and 3.5 percent in recent years. Omaha developers and owners have added close to 1,500 units per year to the supply over the past five years, and demand appears to be keeping pace.

Transaction Volume and Prices

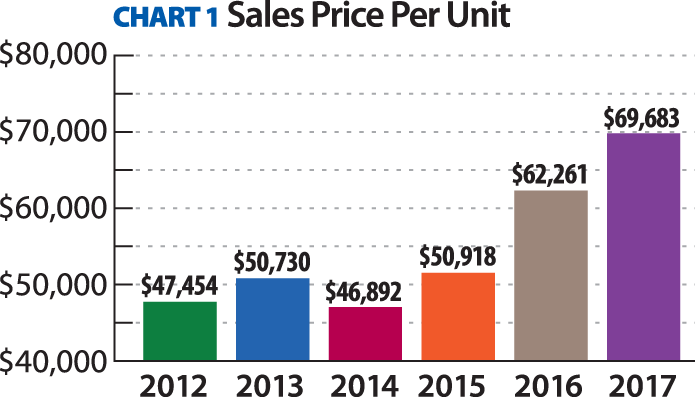

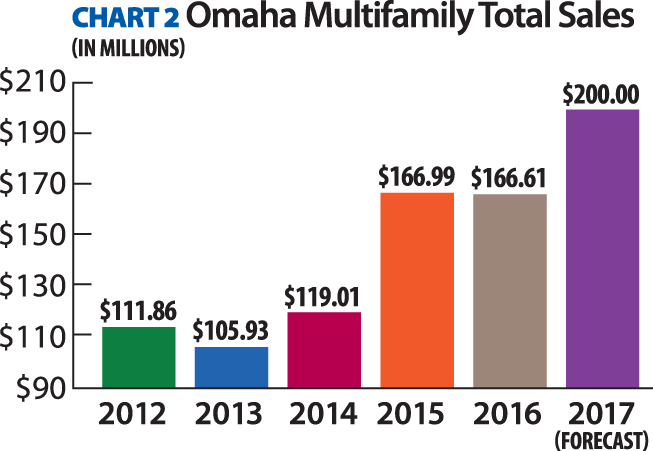

With increased rents, high and stable occupancy, and continued compressed cap rates, the ingredients exist for higher values and robust sales. As indicated in Chart 1, for the years between 2012 and 2014, the average unit sale price in the Omaha metro area was $48,000 per unit. The average sale price per unit in the first half of 2017 was just shy of $70,000, an increase of nearly 45 percent. Total annual sales volume of multifamily averaged $112 million between 2012 and 2014 as shown in Chart 2. The years 2015 and 2016 each had $166 million in transactions, and in the first half of 2017, there was $98 million in multifamily sales. With the pending deals and other projects currently being marketed, it is very likely the Omaha metro area will eclipse $200 million this year – making it a very robust market.

With increased rents, high and stable occupancy, and continued compressed cap rates, the ingredients exist for higher values and robust sales. As indicated in Chart 1, for the years between 2012 and 2014, the average unit sale price in the Omaha metro area was $48,000 per unit. The average sale price per unit in the first half of 2017 was just shy of $70,000, an increase of nearly 45 percent. Total annual sales volume of multifamily averaged $112 million between 2012 and 2014 as shown in Chart 2. The years 2015 and 2016 each had $166 million in transactions, and in the first half of 2017, there was $98 million in multifamily sales. With the pending deals and other projects currently being marketed, it is very likely the Omaha metro area will eclipse $200 million this year – making it a very robust market.

Cap Rates and Product Types

Real Estate Investment Trusts (REITs), private equity groups, family ownerships, and individuals – both local and regional – continue to scour our market for opportunities. The primary and secondary markets are so overheated that capital continues to flow into stable Omaha. For newly built product, it is not uncommon to see sales in the 5.5 percent to 6 percent cap rate range. Additionally, the cap rate spread among older stabilized product, and new product has decreased. For older product, there have been several sales in the mid 6 percent cap rate range, but they were accompanied by upside in rents.

Many older properties burdened with poor management, a lack of understanding of today’s leasing trends and deferred maintenance are selling based on a unit price and not the income approach based on historic numbers. Previous years’ income/expense history is no longer relevant, and a pro forma carries more weight when underwriting value. Experienced buyers find opportunity in these buildings and can manage and rehab their way to a reasonable yield.

There is also strong demand in well-located Class C apartment buildings that are broken, where the rents barely cover – or may not cover – the expenses. These deep value-add projects benefit from an injection of capital, making way for modern amenities and a new tenant mix. Rents may increase by 50 percent to 100 percent after a renovation. These projects offer a greater opportunity to grow rents compared to newly constructed developments, as the cost basis is far less.

Pipeline

In 2017, there will be close to 1,500 units added to the supply, of which about 1,000 will be in Downtown and Midtown. These urban projects include Benson Lights (99), The Yard (110), The Conrad (153), Breakers (214), The Highlander (101), Capitol District (218), The Triangle (137), NICO (48) and Dewey 3700 (24). Significant suburban projects include the Lumberyard District, Park 120 Oak Hills and Avenue 204 at Royal View. In 2018, a second wave of more than 1,000 units will hit the urban market with NuStyle Development’s The Landing, Giddings Group’s The Duke, and projects from GreenSlate Development, Lanoha Development Company, Bluestone Development, Broadmoor, The Vecino Group and Crowe.

This article appeared in our quarterly newsletter from September of 2017. The full newsletter is available at http://files.investorsomaha.com/download/IR_newsletter_Sept_2017.pdf